Speak with our UK equity release specialists:

Speak with our UK equity release specialists: Can I repay my Equity Release?

CertCII (MP & ER)

When considering equity release, you may worry that you will be stuck with a rigid plan for the rest of your life. When advising clients, I am often asked if payments can be made back against an equity release?

Key takeaway

With an equity release plan approved by the Equity Release Council, you can make partial, or full repayment whenever you like. All new plans allow you to make partial payments without charges; however, if you exceed the partial payment limit, you may incur additional fees.

This is one of the many reasons I only recommend equity release plans that meet the Equity Release Council standards.

Launched in 2024, there are now plans which you can repay early in full without incurring any penalty charges (Zero ERC's).

Your equity release offer will show how you can repay your equity release, and if you have an existing plan, you can always check with your equity release provider.

Watch:

Throughout this guide, we will be focussing on the most common type of Equity Release plan, the lifetime mortgage. Currently, lifetime mortgages make up over 99.5% of the new plans we recommend. If you would like further information regarding making payments on other types of equity release, including Home Reversion Plans, please contact us.

How to make partial repayments towards your Equity Release plan

With lifetime mortgages, you can make partial repayments at any time you wish. Payment types include cheque, bank transfer, telephone card payment, standing order, and Direct Debit. You should check with your lender for the latest methods of payment that they currently accept.

All new plans allow you to make partial payments without penalty up to a certain percentage of the amount you borrowed. Even many plans previously sold allow partial payments, too. Typically up to 10% each year, while some plans allow up to 12%, and others 40%. In 2024 we saw the introduction of plans with Zero ERC's allowing you to repay as much as you want without penalty.

The lenders are affording you the flexibility to pay none, some or all of the interest accrued on the plan. You could also make payments above interest charged, allowing you to reduce the capital owed and can save you money when the plan ends.

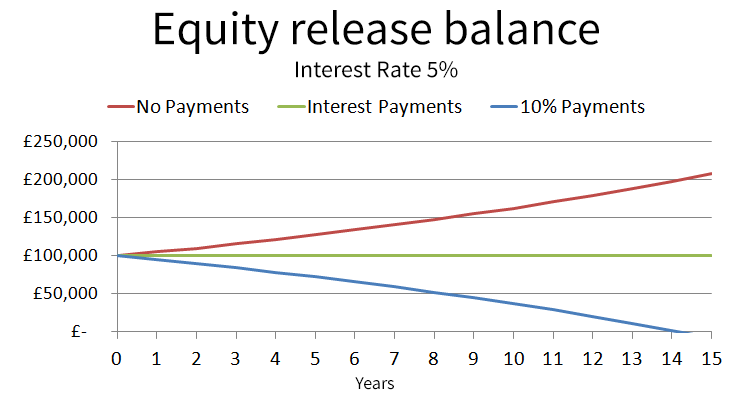

Let's look at a graph showing the impact of making no payments, full interest payments, and 10% overpayments each year.

As you can see, it's possible to repay your equity release plan in full without incurring any penalties by utilising the partial payment feature.

Remember: If you were to make a repayment above your plan's allowance, you might incur an early repayment charge (ERC). These include administration charges, and also for the potential loss in income the lender will make by you reducing the capital owed.

If you are thinking about making payment against your equity release, it may be beneficial to seek advice from your equity release advisor.

What happens when you repay your Equity Release plan in full?

Equity Release plans are designed to run until the death of the last borrower, or when the last borrower moves into long-term residential care. At the end of the plan, the lender will be repaid for the capital and interest accrued.

Despite this, you can make payments against the Equity Release plan, or repay it in full at any point in time.

However, when making repayments, you may incur an Early Payment Charge.

What are Early Repayment Charges (ERC's) on an equity release?

Early Repayment Charges (ERC's) are additional fees charged by your lender for making repayments on the plan outside of any pre-agreed allowances. The charges levied are designed to cover the losses the lender has occurred by you repaying sooner than they expected.

Different lenders with different plans levy charges in different ways, so it is essential you understand any charges associated with your plan.

Equity release plans with Fixed-Rate ERC's

The most significant benefit of fixed-rate ERC's is that you know exactly what rate ERC is charged before you sign any legal paperwork for the plan. Meaning that there are no nasty surprises later if you wish to make payments back on the plan.

Canada Life offer fixed-rate ERC's on plans, an example of their charges on some of their plans can be seen below:

Canada Life state:

Payments can be made at any time. After any ERC free exemptions, you will be charged an ERC on the amount that is repaid.

| Years | Percentage ERC on the amount repaid |

| 1 | 5% |

| 2 | 5% |

| 3 | 5% |

| 4 | 5% |

| 5 | 5% |

| 6 | 3% |

| 7 | 3% |

| 8 | 3% |

| 9 onwards | 0% |

Variable-Rate ERC's

With variable-rate ERC's, you do not know what charges will be levied until you make any payment. All variable rate ERC's must have an upper limit to meet the Equity Release Council product standards.

Aviva offer variable-rate ERC's on their plans, let's look at an example of their charges below:

Maximum ERC of 25% of the initial amount borrowed.

Minimum ERC of 0%.

Aviva state:

We calculate this charge based on the movement in gilt redemption yields between the date the lifetime mortgage completed and the date you are quoted an early repayment charge. A gilt is a Government security and a number of different gilts are available. The specific gilt associated with your lifetime mortgage is chosen to reflect its expected term. You will incur an early repayment charge if the gilt yield is lower on the date you are quoted an early repayment charge than on the date the lifetime mortgage completed. Where we quote you an early repayment charge it will be valid for 3 working days, including the day the figure is quoted. This is explained more fully in your terms and conditions booklet.

As you can see, with Aviva plans, you could potentially pay no additional charges for repaying early. However, if you repay in the first few years, you could be charged far more in Early Repayment Charges, than for the interest that could have accrued!

However, Aviva also offer fixed-rate ERC's if you would prefer the certainty of knowing what the penalty would be.

It is essential that you discuss your plans to repay with your equity release with your advisor prior to taking out any equity release plan.

ERC's on Initial Borrowing vs Balance

When comparing plans, it is important to know that some lenders base ERC's on the initial borrowing, while others calculate it on the current balance outstanding. This could potentially have a significant impact on the ERC that is charged, depending on when you make the payment.

For example, if you borrowed £100,000 at 5% AER, the amount owed after four years has grown to £121,551.

With an ERC penalty of 5% of initial borrowing, the maximum ERC is £5,000.

With an ERC penalty of 5% of the balance owed, the maximum ERC is £6,078.

How to find out how much any Early Repayment Charge (ERC) will be

The easiest ways to find out how ERC's are charged on your plan are by checking your mortgage contract document, or by contacting the lender directly.

Once you understand how the charges are calculated, you should know if any charges are likely to be incurred for payments you are planning to make.

An equity release adviser can help you if you are unsure of charges the lender will make.

At the point of making payment to the lender, you should request details of any charges they are imposing, and how much you are reducing the balance owed.

Circumstances in which Early Repayment Charges (ERC's) do not apply

You will never be asked to pay an early repayment charge if you repay following the death of the last borrower, or if the last borrower moves into long-term care. If you make payments back on your plan before this, you may be charged an ERC. Below we have listed common ERC exemptions which are included in some plans. If you believe you may make payments back on your plan before the natural term end, you should discuss this with your equity release advisor.

Overpayments

All lenders offer plans which allow you to make partial repayments without incurring ERC's. They are often on an informal basis where they enable you to make payments but are not required.

We have already discussed how some lenders offer plans which allow up to 10% repayment each year, while some plans allow up to 12%, and others 40%.

But this isn't the only difference. Some lenders allow you to make unlimited payments from day one. However, other lenders will set the maximum frequency of payments and require the plan has run a minimum time.

Let's look at an example of overpayment exemption offered by Aviva on a new plan.

Aviva state:

Each year, the maximum amount you can repay is 10% of the initial loan, including any additional borrowing and cash reserve releases, excluding any accrued interest. There is no limit to the number of repayments you can make in a year, but each instalment must be a minimum of £50.00.

Porting your plan when moving property

All lifetime mortgages that meet equity release council standards are portable. This means that you may transfer your lifetime mortgage to a new property when moving, providing that the new property matches your lender's property criteria.

You can use the sale proceeds of your property to pay your equity release back in full when you move to a new home. However, you may incur an early repayment charge.

Moving house doesn't always mean you need to pay your plan back in full. Instead, you can port your existing plan to a new property. All lenders that are part of the Equity Release Council allow you to do this as long as the lender approves of the new property for their lending criteria.

Please note: If the new property is significantly lower in value, your lender may require you to repay part of your mortgage balance.

For example, if you were moving to a property which was 50% of the value of your existing property, you may be requested to pay 50% of the amount owed to the lender. This is because their security has dropped by 50%. This shouldn't be a problem as; hopefully, you will have enough to cover the required payment from the sale proceeds of your existing home.

Let's look at an example of an exemption offered by Aviva on a new plan.

Aviva state:

If you move home and want to transfer this lifetime mortgage to your new property, you can do so if your new property meets our lending criteria at the time of your application. You will have to pay an application fee but not an early repayment charge. See Section 11 for more information on fees. If your new property is of a lower value, we may ask you to repay part of the amount you owe. If you move home and your new property does not meet our lending criteria, you must repay this lifetime mortgage. You may have to pay an early repayment charge. See Section 13 for early repayment charges. If you are eligible for downsizing protection you will not have to pay an early repayment charge. Whether or not you can benefit from downsizing protection depends on your circumstances and is more fully explained in the terms and conditions booklet

It's also worth noting that different lenders have different underwriting criteria. So while your new property may not meet criteria for your existing lender, you still may be able to get equity release with another lender.

I have written a complete guide on moving home with equity release, which you can read to understand the process fully.

Downsizing Protection

Downsizing protection is another excellent exemption offered by some lenders. This exemption which allows you to pay your equity release back early when you move home, without incurring any early repayment charge.

As the name suggests, it's often used when you downsize and move to a new property that is lower in value. However, it could be that you move to a larger property or a property higher in value.

Different lenders have variations for this feature. A notable difference between lenders is that some will only let you use downsizing protection when they don't approve of the new property. Other lenders allow you to use it at any point, regardless if they are willing to port your existing plan.

Another difference amongst lenders is some of them offer you to be able to use the feature from day one. However, other lenders won't allow it to be used until a set amount of time has passed – typically after five years. It's essential you understand the feature fully for any plan that is recommended to you, and especially if you plan to use it.

Canada Life offer Downsizing Protection on plans; please see an example of this feature below.

Canada Life state:

An early repayment charge is not payable if you repay the lifetime mortgage after 5 years as a result of selling your home and moving to a different property.

Significant Life Event exemption

Let's look at an example of an exemption offered by Aviva on a new plan.

Aviva state:

Early repayment charges do not apply if you have a joint lifetime mortgage and you repay within three years of the date that one of you has died or the date that you notify us that one of you needs long-term care.

Do I need to make payments towards my Equity Release plan?

With all lifetime mortgages, you are not required to make mandatory payments while you are alive.

What's more, all lifetime mortgages approved by the equity release council require that the lender cannot ask for the money back early in any circumstance. Even if property prices crash, interest rates spike or the lender ceases to trade. You will always be able to live in your home for as long as you wish.

We work with equity release brands you can trust

Throughout this guide we have looked at examples from a few lenders, but they are not all that we work with. Find out more about lenders and plans specific to you by booking your FREE equity release consultation.

If you have further questions, why not speak with one of our qualified advisors?

Call us on 0207 158 0881 or use our online form to book your FREE consultation.

This guide is for information only and does not constitute financial or legal advice.

Equity release may involve a lifetime mortgage or home reversion plan and is not suitable for everyone.

It can reduce the value of your estate and may affect your entitlement to means-tested benefits.

To understand the full features and risks, ask for a personalised illustration.