Speak with our UK equity release specialists:

Speak with our UK equity release specialists:

CertCII (MP & ER)

How do you calculate equity release compound interest?

The easiest way is to use our compound interest calculator (above). However, you can also use Excel.

To calculate the compound interest on equity release, you require the loan amount, the interest rate, and the number of years to compound the interest. To calculate the total amount owed in Excel, you can use the following formula: =FV([Annual Interest Rate],[Years],[Annual Payments], -[Loan Amount],0)

Let's look at an example.

Calculating Compound Interest In Excel Example

Loan Amount: £50,000

Interest Rate: 6%

Annual Payments £0

Compound Years: 15

Excel Formula: =FV(6%,15,0,-50000,0)

Resulting total owed after 15 years: £119,828

But, rather than using Excel, let's explore how to use our compound interest calculator.

Property value

When considering any equity release, your property value significantly impacts the amount you can borrow and the interest rate the lender will charge.

Furthermore, the impact of any property growth is also on the whole value of your home.

Our compound interest calculator uses your property value to find your interest rate and calculate the potential retained equity in your home.

Please submit your property value in pounds, e.g. £300,000.

Age of youngest homeowner

The age of the youngest homeowner allows us to estimate how long the equity release plan may last.

Most lenders calculate average life expectancy as 87 years. Therefore, at 55, the estimated term is 32 years.

We estimate the minimum plan term to be 15 years, even when you are over 72 years old.

Do you know your interest rate?

If you know the interest rate for your equity release plan, you can enter it here. But don't worry if you don't know the interest rate you are likely to achieve.

We can search the market to find out what interest rate you are likely to achieve. All we need is:

- how your property is owned (single or jointly)

- your property type

- the country your property is in

- your release amount

The interest rate quoted may not be the final rate you receive, but it will give you a good indication.

When ready, you can speak with one of our equity release advisors to receive your personalised rate. This rate could be higher or lower than the one our calculator provides.

MER vs AER

Most equity release lenders express interest rates as Monthy Equivalent Rates (MER).

However, some lenders show Annual Equivalent Rates (AER) rates.

Because interest compounds monthly, if you have an MER but choose not to make any payments, the interest after the first year will be more than the loan multiplied by the interest rate.

Our calculator can take in either an MER or an AER.

Drawdown lifetime mortgages

A significant benefit of a drawdown lifetime mortgage is the option to have a reserve facility.

Money held in reserve does not attract interest, and you can typically request a minimum of £2,000 for each tranche.

The interest rate that you achieve will depend on the total facility required.

When borrowing from the reserve, each additional tranche will have a separate interest rate, fixed to the prevailing rate at the time of request.

For our compound interest calculator, we assume the same interest rate for all borrowing.

Making optional payments

If you choose to make optional payments, they will help mitigate the interest that compounds on the loan.

However, it is unusual to recommend that you make payments and have a reserve. So, with the calculator, you can either have a drawdown plan or make monthly payments.

If you require both, please speak with one of our equity release advisors for a bespoke forecast.

Equity release balance over time

When calculating your results, you will see that we show the balance owed each year over the estimated term.

The natural term end is when the last homeowner passes away or moves into care - so your loan will still increase if you are still living in your home after the estimated term.

Interest only stops accruing once the balance is repaid in full.

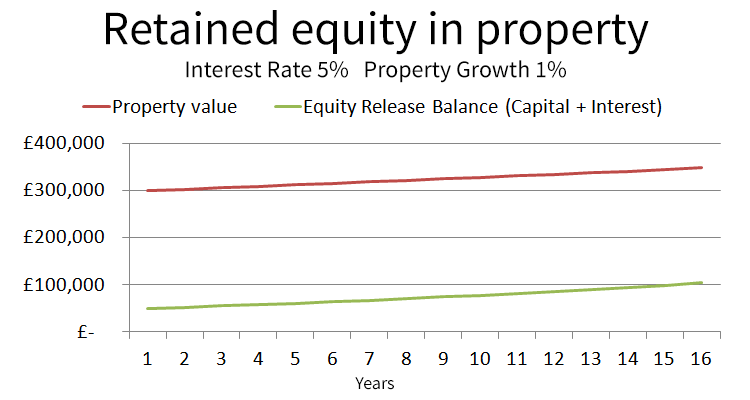

The impact of potential property growth

While interest on a lifetime mortgage compounds if you do not make any payments, any changes to your property value do, too.

Our compound interest calculator shows a 3% annual growth impact on your property value.

You can then see how much equity could be retained in your property.

Let's look at an example of retained equity in a home.

As you can see, while the equity release interest is compounding in nature, so is any growth on the property.

Most people have seen steady property growth in the past, and expect to see increases in the future too.

In our example, the retained equity in the property (property value - equity release balance) increases yearly despite the equity release interest rate being higher than the property growth percentage rate.

Important: While the equity release interest rate is higher than the property growth rate, the lender only charges interest on the equity release balance. Whereas, any increases on the property are on the total property value.

If you need help using our compound interest calculator or want to see other forecasts, please contact us for your personalised illustration.

If you have further questions, why not speak with one of our qualified advisors?

Call us on 0207 158 0881 or use our online form to book your FREE consultation.

While a qualified equity release advisor has written this guide, it is not intended to be used as financial nor legal advice and should not be relied upon.

Equity release is not right for everyone and may involve a lifetime mortgage or home reversion plan.

If you are considering Equity Release we recommend you read through is equity release right for me? carefully.

We have also created a Myth Buster for further useful reading.

Equity release can impact your entitlement to mean tested benefits and will impact the value of your estate.

To understand the full features and risks of an Equity Release plan, ask for a personalised illustration.