Speak with our UK equity release specialists:

Speak with our UK equity release specialists: Equity Release Plans Without Rolled-Up (Compound) Interest

CertCII (MP & ER)

One of the attractions of an equity release plan is that there are no mandatory monthly payments. But a downside of letting interest 'roll-up' without repayment on a lifetime mortgage is compounding interest (interest charged on top of interest already accrued).

This is one of the main reasons why people do not like equity release plans. But is there an option to take an equity release without the compound interest?

Key takeaway

There are two types of equity release plan which do not have compound interest. An interest serviced lifetime mortgage; You repay the interest monthly, and the capital at the end of the plan. A Home Reversion Plan does not attract interest; instead, the reversion provider has a percentage share ownership of your home.

But what are the drawbacks of an equity release plan that does not have compound interest over a roll-up plan? Let's explore the differences in more detail.

How does roll-up compound interest work on a lifetime mortgage?

The most popular form of equity release is a lifetime mortgage. All lifetime mortgage lenders offer 'roll-up' plans. With a 'roll-up' lifetime mortgage, the interest accrued does not need to be repaid each month and instead it is added to the loan balance.

The interest charged can be expressed as an Annual Equivalent Interest Rate (AER). At the end of the first year, the interest charged will be equal to the AER multiplied by the original loan amount. At the end of year two, the interest is charged on both the initial capital borrowed, and also the interest accrued in year one. This continues throughout the life of the plan and is known as compounding interest.

With a lifetime mortgage that meets the Equity Release Council standards, your interest rate will be fixed for life. But, although the interest rate is fixed, the annual interest charged will become larger each year that the mortgage runs.

Let's look at an example of how compound interest accrues at a fixed rate of 6% AER on a £100,000 roll-up lifetime mortgage:

| Year | Opening Balance | Interest Charged | Closing Balance |

| 1 | £100,000 | £6,000 | £106,000 |

| 2 | £106,000 | £6,360 | £112,360 |

| 3 | £112,360 | £6,742 | £119,102 |

| 4 | £119,102 | £7,146 | £126,248 |

| 5 | £126,248 | £7,757 | £133,823 |

| 6 | £133,823 | £8,029 | £141,852 |

| 7 | £141,852 | £8,511 | £150,363 |

| 8 | £150,363 | £9,022 | £159,385 |

| 9 | £159,385 | £9,563 | £168,948 |

| 10 | £168,948 | £10,137 | £179,085 |

| 11 | £179,085 | £10,745 | £189,830 |

| 12 | £189,830 | £11,390 | £201,220 |

| 13 | £201,220 | £12,073 | £213,293 |

| 14 | £213,293 | £12,798 | £226,090 |

| 15 | £226,090 | £13,565 | £239,656 |

| 16 | £239,656 | £14,379 | £254,035 |

| 17 | £254,035 | £15,242 | £269,227 |

As you can see, the more years that the plan runs, the more significant the interest charges are in the year.

While lifetime mortgages are available from age 55, you should remember that the younger that you are, the longer the plan will typically run. As such, younger borrowers are more at risk from compounding interest than older borrowers.

Regardless of your age, if you are considering an equity release, you could mitigate the effects of compound interest by servicing the interest as it accrues on your plan.

Servicing the monthly interest on an equity release plan.

There are options available to help avoid the compound interest building up. One of those is to pay the interest each month so that it isn't added to the mortgage balance.

Suppose you were to service the interest over the full duration of the lifetime mortgage. In that case, you could potentially only owe the amount you initially borrowed at the end of the term. This is known as an interest serviced lifetime mortgage.

You may also receive a reduction to the interest rate for servicing the interest.

With interest serviced plans, you make regular monthly payments (often by direct debit). As the interest rate will be fixed for life, the payments you would make stay the same too.

Unlike a residential mortgage, if for any reason you are in the future unable to make the monthly payments, there is no risk to your home.

Should you wish to stop making payments you can:

Take a payment holiday – Many interest-serviced lifetime mortgages allow you to skip your monthly payments. With a Just For You interest services lifetime mortgage from Just retirement, you are entitled to one request for a payment holiday of 3 consecutive months each year.

Switch to roll-up – Alternatively, if you stop the monthly payments at any point during the life of the mortgage, the plan will revert to 'roll-up'. If you received a reduction to your interest rate, this would now increase to the roll-up rate applicable. Also, once direct debit payments have stopped, they cannot then be restarted. You should check with your particular lifetime mortgage, as you will usually still be able to make ad-hoc voluntary payments.

Please note: You can choose the monthly payment you make at the outset, whether that is all or part of the interest charges. Ultimately the amount that you agree to pay will significantly depend on how much you are happy to commit to, and can afford.

Can I pay off some of the interest without making regular monthly payments?

With many roll-up lifetime mortgages, there is also the option to make ad-hoc voluntary payments to the plan; similar to a residential mortgage.

Different lifetime mortgages have different rules in the amount in voluntary payments that may be paid each year, the frequency and the minimum amount for each payment. On average, you will be able to pay up to 10% of the initial amount borrowed in any 12 months, from the day your application completes, without incurring an early repayment charge (ERC).

There is currently one lender available who offers the opportunity to pay up to 40% of the initial loan in voluntary payments in year 12 month period. You are also able to spread that amount into 12 monthly payments if you choose, subject to a £500 minimum per payment.

The voluntary payment option allows you the freedom to decide to repay to keep the compound interest down or to enjoy the extra cash while you are still alive.

Any payments that you make are purely voluntary, and there is no risk of repossession of your home if you choose to pay nothing until the end of the plan.

Why Home Reversion Plans do not have compound interest.

With a home reversion plan you are not charged interest, so there will be no compounding interest to be concerned. However, the most considerable downside with a reversion plan is that you sell a percentage of your property to receive the cash from the reversion provider.

Therefore with a home reversion plan, you will no longer retain full ownership of your property, making it harder to move in the future. You will also benefit less from any positive house price movements.

Home reversion plans are still available; however, because of these significant drawbacks, they make up less than 1% of the equity release market.

If you are considering taking a home reversion plan to mitigate compound interest, put us to the challenge to find you a more cost-effective lifetime mortgage!

How changes to the value of your home are compounded too.

When you look at compound interest charges on a roll-up lifetime mortgage, it is also worth remembering that any increases in property prices are compounded too. And this can affect the amount left over for you or to your estate after the mortgage is repaid.

Example based on a property value of £185,000:

If your home went up in value by 1% each year, it would be worth £219,096 after 17 years.

If your home went down in value by 1% each year, it would be worth £155,944 after 17 years.

This is an example only and is not how much the value of your home will change.

An area of concern you may have is that if the value of your property goes down, how will your beneficiaries repay the balance owed?

With all plans that meet the Equity Release Council standards, neither you nor your beneficiaries will owe more than your properties worth. You are protected by the 'no negative equity' guarantee.

Upon your death or (if a joint plan) on the death of the second borrower, or if you need to move into long term care, if the value of your home is not enough to repay what you owe on your lifetime mortgage, the lender will be responsible for absorbing the difference.

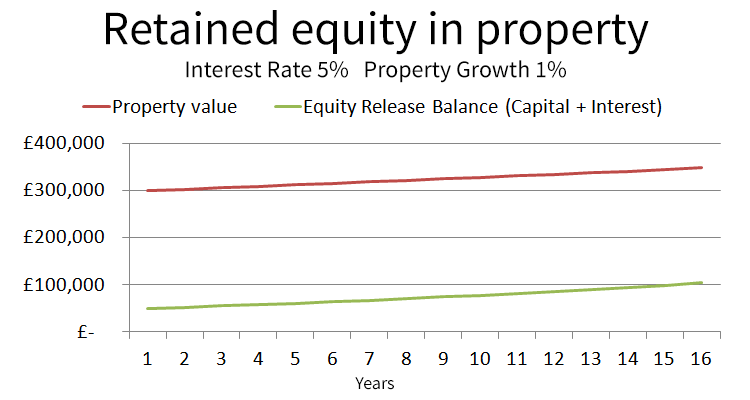

Alternatively, if your properties value increases, you will be able to benefit more than with a home reversion plan. Let's look at an example:

As you can see, while the equity release interest is compounding in nature, so is any growth on the property.

Most people have seen steady property growth in the past, and expect to see increases in the future too.

In our example, the retained equity in the property (property value - equity release balance) increases year on year, despite the equity release interest rate being higher than the property growth percentage rate.

But why is this?

This is because while the equity release interest rate is higher than the property growth rate, the lender is only charging interest on the equity release balance. Whereas, any increases on the property are on the total property value.

In our example, the release value is 1/6 of the property value. This means that in year one, the interest of 5% is actually less than 1% of the property value (100% / 6 * / 5% = 0.83%).

So as you can see, even with compound interest, a roll-up plan may still offer you good value.

If you have further questions, why not speak with one of our qualified advisors?

Call us on 0207 158 0881 or use our online form to book your FREE consultation.

This guide is for information only and does not constitute financial or legal advice.

Equity release may involve a lifetime mortgage or home reversion plan and is not suitable for everyone.

It can reduce the value of your estate and may affect your entitlement to means-tested benefits.

To understand the full features and risks, ask for a personalised illustration.