Speak with our UK equity release specialists:

Speak with our UK equity release specialists: Do you have equity release? You could save £30,000* by switching plan.

CertCII (MP & ER)

Key takeaway

If you took out equity release more than 12 months ago, you could save thousands of pounds by switching to a lower interest rate equity release plan. Our clients have saved over £30,000* on average by switching.

Entering into an equity release agreement is a big decision to make, and the plans are designed to be with you for the rest of your life. But this does not mean that it should be a "setup and forget" arrangement.

Interest rates for lifetime mortgages (the most popular form of equity release) changed each year. The Equity Release Council has reported that the average interest rate for a lifetime mortgage arranged in 2019 was 4.91%. In 2016, only three years earlier, the average interest rate was 5.96%. This means that there are thousands of existing equity release clients who could be paying over the odds for their equity release plan.

You can check the latest interest rates available here.

How do you know if you are overpaying on your existing equity release?

There isn't a quick way for you to personally calculate savings on plans with lower interest rates that are more suitable though. That is where we step in. We offer a free equity release review, whereby we produce a report detailing any potential amounts of money that you could save by switching. We also provide you with details of any extra funds which you could release.

So far, of the existing plans that we have reviewed, we have been able to highlight savings for more than 100 clients!

The savings that we can unlock are potentially tens of thousands of pounds!

Imagine the difference that could make; being able to access further funds without costing you more or being able to pass the savings onto your loved ones.

How much could I save by switching to a new plan?

When considering how much you could potentially save, we first examine your current equity release plan and why it was originally recommended to you. This includes taking into consideration your circumstances, along with any property underwriting criteria which may have been considered.

We then request a current balance from your existing provider, along with details of any early repayment charges. This gives us an amount of money to source from the broader market to see if there are any lower interest rate plans available.

The final step is to forecast how long you, and the lender, expects the plans to last. We can then consider the expected total cost over the term, and therefore can provide details of any potential savings to be made over the lifetime of the plan.

Let's look at an example:

MR AND MRS SMITH

Aged: 62 and 63

EXISTING PLAN

Plan arranged: April 2017

Interest rate: 4.20% AER

Balance: £62,860

Estimated term remaining: 25 Years

NEW LOWER RATE PLAN

Interest rate: 2.92% AER

TOTAL SAVINGS OVER ESTIMATED TERM

£32,857

Even if interest rates have risen, it is a sensible idea to review plans annually. Interest rates regularly change and so could your circumstances.

We have also seen more and more new equity release plans coming to market, often with additional features and more flexible underwriting. This means that clients who were previously restricted on lenders, and potentially the features they could obtain, are now able to access much better plans.

Examples of additional features

Significant life event exemption. This exemption affords you the flexibility to repay the mortgage without penalty within three years of the death of the first borrower, or the first borrower entering permanent long term care. I have found this feature a high-value proposition when advising clients who are looking to make a joint application.

Downsizing protection. Different lenders offer this protection in different ways. The feature can mitigate any early repayment charges which could arise when downsizing to a new property in the future. Typically this comes into place five years after the equity release plan has been arranged; however, some lenders offer it sooner. Some lenders offer this to clients who wish to move to a new property which doesn't meet their lending criteria. While others provide this feature to clients when selling their property.

Making optional payments. This has been available on several plans in the past. However, lenders are now required by the equity release council to offer new plans with options to make payments without incurring penalty charges. There are even lenders offering discounts on the lifetime mortgage interest rates if you opt to make regular payments against interest which is charged.

Examples of flexibility with underwriting

Some lenders will now lend on properties that have an element of personal commercial use (under 50% of the total property to be secured)

This means they can now lend on:

- Properties with a small home-based business

- Homes with a tenant, with a suitable tenancy agreement

- Homes where one or two rooms within the main home or a self-contained part used for B&B and holiday lets (inc Airbnb)... guest stay mustn't be beyond 30 consecutive days

- Houses with land and buildings in personal agricultural or equestrian use

Changes also include an increased range of property types from historic to modern methods of construction, including:

- Modern Eco homes

- Thatched properties including grade I and II* and many historic building techniques

- Basement flats

- Studio flats

What if I took out my equity release in the last 12 months?

Even if you recently took out your equity release plan, you still may be able to make savings or borrow additional funds. It is essential to review your circumstances regularly and to consider how any of your plans have changed.

So, even if your review shows your current plan is the best for you to keep, your time is not wasted. Remember: Money Release will not recommend any new finance arrangement if it is not in your best interest to take it out.

What's more, we can keep you updated on any future market developments and any new plans which may be able to save you money in the future too.

What if I have Early Repayment Charges to pay?

If you pay back an existing equity release plan before the natural term end, you may incur additional charges called Early Repayment Charges (ERC's). These charges generally fall into two main types:

- Fixed-rate ERC's

- Variable-rate ERC's

With fixed-rate ERC's, you will find that there is a known percentage that the lender will charge for you to pay back early. They can be charged as a percentage on the amount you initially borrowed, or as a percentage on the amount you are repaying.

In either scenario, you are likely going to be charged somewhere between 3% and 6%, with the maximum we have seen of 10%.

With variable-rate ERC's, the penalty is likely to be linked to a GILT. As the name suggests, the variable nature means that you do not know what any potential penalty would be without contacting your existing lender. They then calculate the amount owed to repay early. We have seen some plans that can be repaid without incurring any ERC's, while others could be up to 25% of the initial amount borrowed.

While these charges are potentially significant, a small decrease in interest rate can potentially save you thousands in compound interest, offsetting these additional charges very quickly.

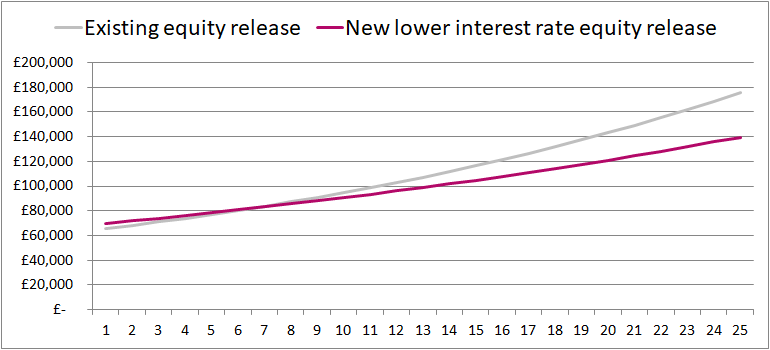

Let's look back at our earlier example to see how the charges affect the savings over the term. On the x-axis is years; the y-axis is the balance of the plan.

As you can see, the requirement to borrow additional monies does mean that in the first few years the new plan is more expensive than retaining the old one. However, the crossover point is during year seven and the saving from then on in mount up significantly.

So even if you are required to pay a penalty for settling your existing equity release plan early, you may still be able to save a significant amount of money over the life of the new plan.

What do you need to see if there are potential savings to be had?

The good news is that we do all the hard work for you. All we require from you is permission to speak to your existing equity release lender and to run through some basic applicant and property criteria with you.

We then produce a full report detailing the amounts you may be able to save, along with the additional cash you may be able to release too.

After you have reviewed your report, your advisor will be able to explore your current circumstances further, and your plans for the future. They will then be able to provide their recommendation for any new plan that may be more suitable for you.

If following your recommendation you wish to proceed, we complete all the necessary paperwork with you and apply to the lender. The rest of the process should be reasonably similar to the first time you took out an equity release plan. The exception is that your solicitor will redeem your existing equity release with your current lender. If any additional funds were requested, your solicitor would transfer these to your bank account directly.

So put us to the challenge and see if you too could save thousands of pounds by switching your equity release plan today. Complete our webform, and we will be in touch to produce your report.

If you have further questions, why not speak with one of our qualified advisors?

Call us on 0207 158 0881 or use our online form to book your FREE consultation.

This guide is for information only and does not constitute financial or legal advice.

Equity release may involve a lifetime mortgage or home reversion plan and is not suitable for everyone.

It can reduce the value of your estate and may affect your entitlement to means-tested benefits.

To understand the full features and risks, ask for a personalised illustration.